Financial planning for low income earners often seems like an impossible task. Many believe that budgeting and saving are luxuries reserved for those with higher incomes.

At Pro Hockey Advisors, we know this couldn’t be further from the truth. Creating a solid financial plan is not only possible on a low income, but it’s also essential for building a stable future and achieving your goals.

Assess Your Current Financial Situation

Calculate Your Total Monthly Income

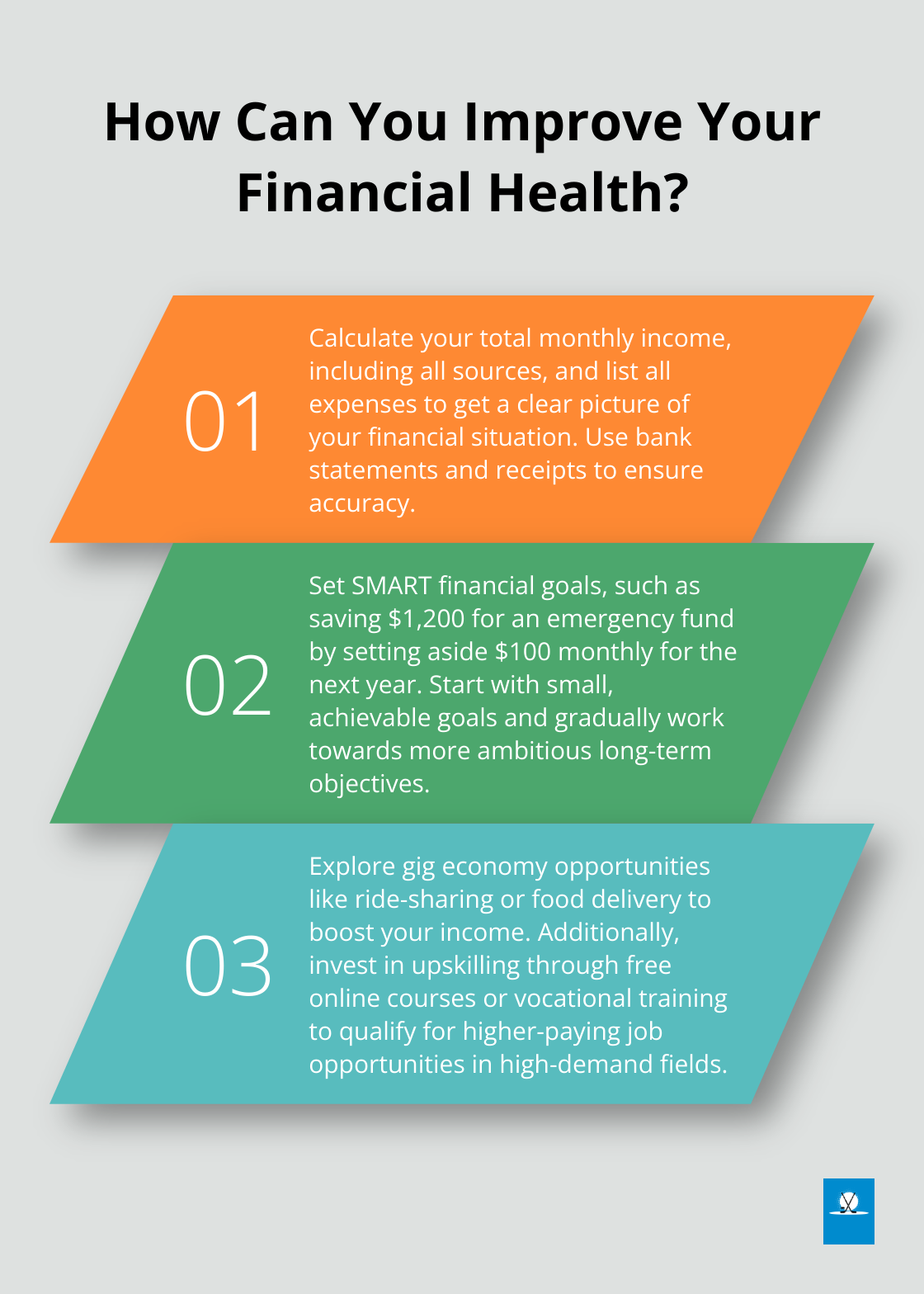

Start your financial plan by calculating your total monthly income. Include all sources of money: your primary job, part-time work, government assistance, and side hustles. Use your adjusted gross income (AGI), which is your total income minus certain adjustments allowed by the IRS. This represents the actual amount you have to work with.

List All Monthly Expenses

Next, create a comprehensive list of your monthly expenses. This should include fixed costs (rent, utilities, loan payments) and variable expenses (groceries, transportation, entertainment). Use bank statements and receipts to ensure accuracy.

Identify Areas to Cut Costs

After you have a clear picture of your spending, look for areas where you can reduce expenses. Focus on non-essential costs that you can minimize or eliminate. Try using cash for discretionary spending to make it more tangible and easier to control.

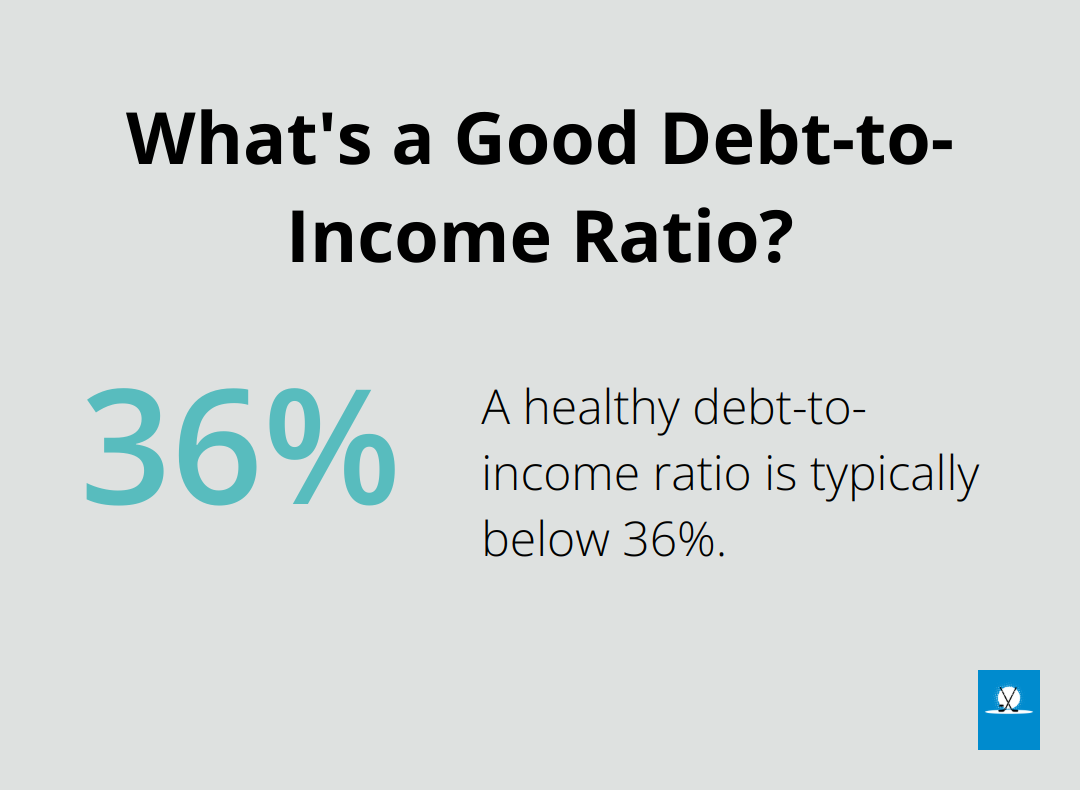

Determine Your Debt-to-Income Ratio

Calculate your debt-to-income ratio by dividing your monthly debt payments by your gross monthly income. This ratio helps you understand how much of your income goes towards debt and determines your borrowing risk. A healthy debt-to-income ratio is typically below 36%. If yours is higher, prioritize paying down debt in your financial plan.

Understanding your financial standing leads to better decision-making and goal-setting. These steps lay the groundwork for a solid financial plan, even on a low income. The key is to be honest with yourself about your finances and commit to making necessary changes.

Now that you have a clear picture of your financial situation, it’s time to set realistic goals that align with your income and aspirations. Let’s explore how to establish achievable financial objectives in the next section.

Setting Goals That Match Your Income

Start Small, Think Big

When you’re on a low income, setting financial goals can seem overwhelming. Start with small, easily achievable short-term goals. Save $50 a month or pay off a small debt. These quick wins will build your confidence and momentum. As you progress, set more ambitious long-term goals, such as building a six-month emergency fund or saving for a home down payment.

Prioritize Based on Your Needs

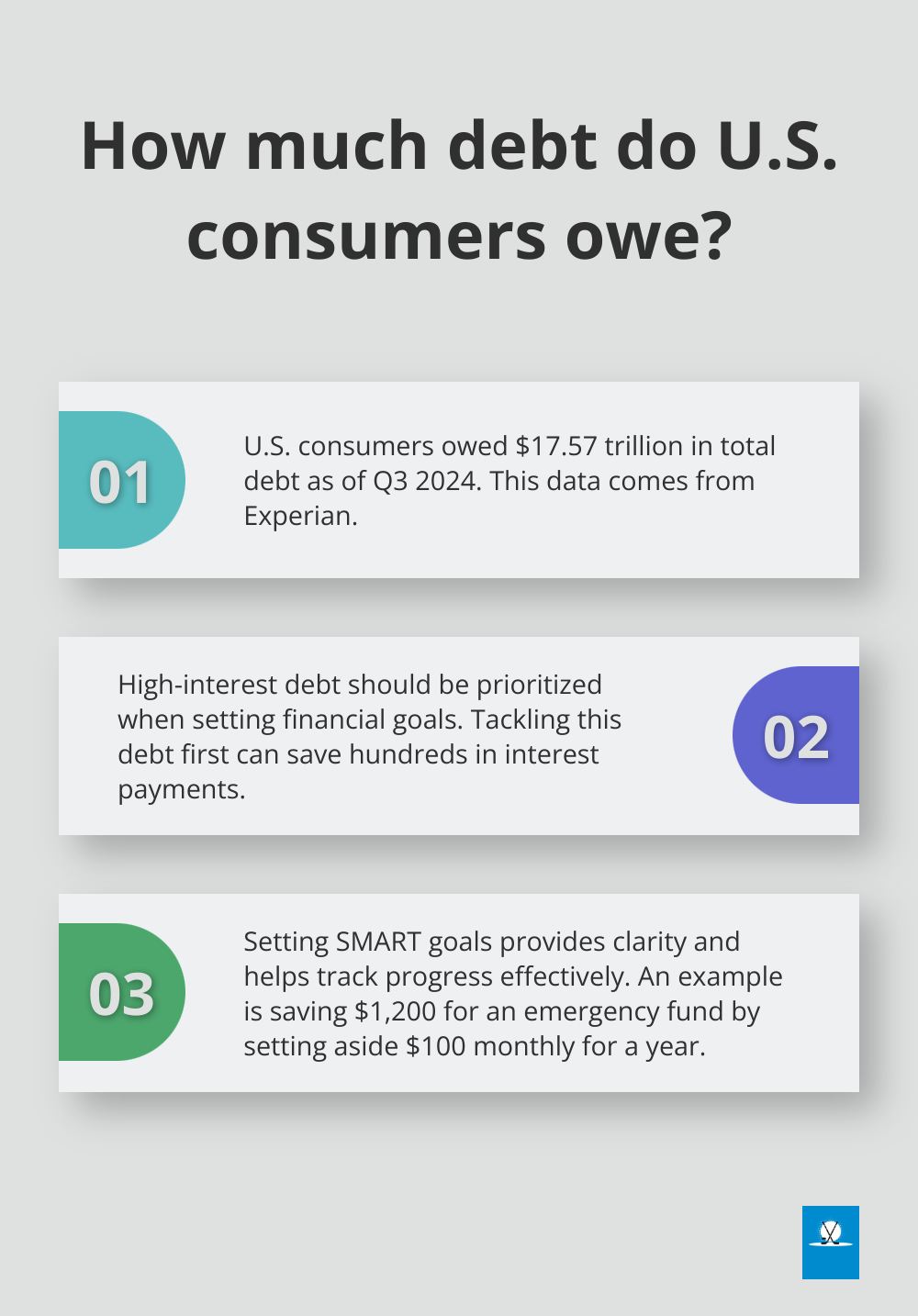

Not all financial goals hold equal importance. Assess which objectives are most urgent for your situation. For many, paying off high-interest debt should take precedence over other savings goals. Consumers in the United States owed $17.57 trillion in total debt as of the third quarter (Q3) of 2024, according to Experian data. Tackle high-interest debt first to save hundreds in interest payments.

Create SMART Goals

Vague goals like “save more money” are difficult to achieve. Instead, make your goals Specific, Measurable, Achievable, Relevant, and Time-bound (SMART). For example, “Save $1,200 for an emergency fund by setting aside $100 monthly for the next year” is a SMART goal. This approach provides clarity and helps you track your progress effectively.

Align Goals with Your Life Plan

Your financial goals should reflect your lifestyle and future needs. If you plan to start a family or change careers, factor these life changes into your financial planning. Overall annual expenses averaged about $300 less for children from birth to 2 years old, and averaged $900 more for teenagers between 15-17 years old. Understanding such potential expenses helps you set realistic long-term financial goals.

Review and Adjust Regularly

Goal-setting is an ongoing process. Review and adjust your objectives as your income and circumstances change. This flexibility allows you to adapt to new opportunities or challenges that arise. Try to reassess your goals at least twice a year to ensure they remain relevant and achievable.

With persistence and the right strategy, even those on low incomes can achieve significant financial milestones. Now that you’ve set clear goals, let’s explore effective strategies to maximize your income and turn these goals into reality.

Boosting Your Income: Practical Strategies

Leverage the Gig Economy

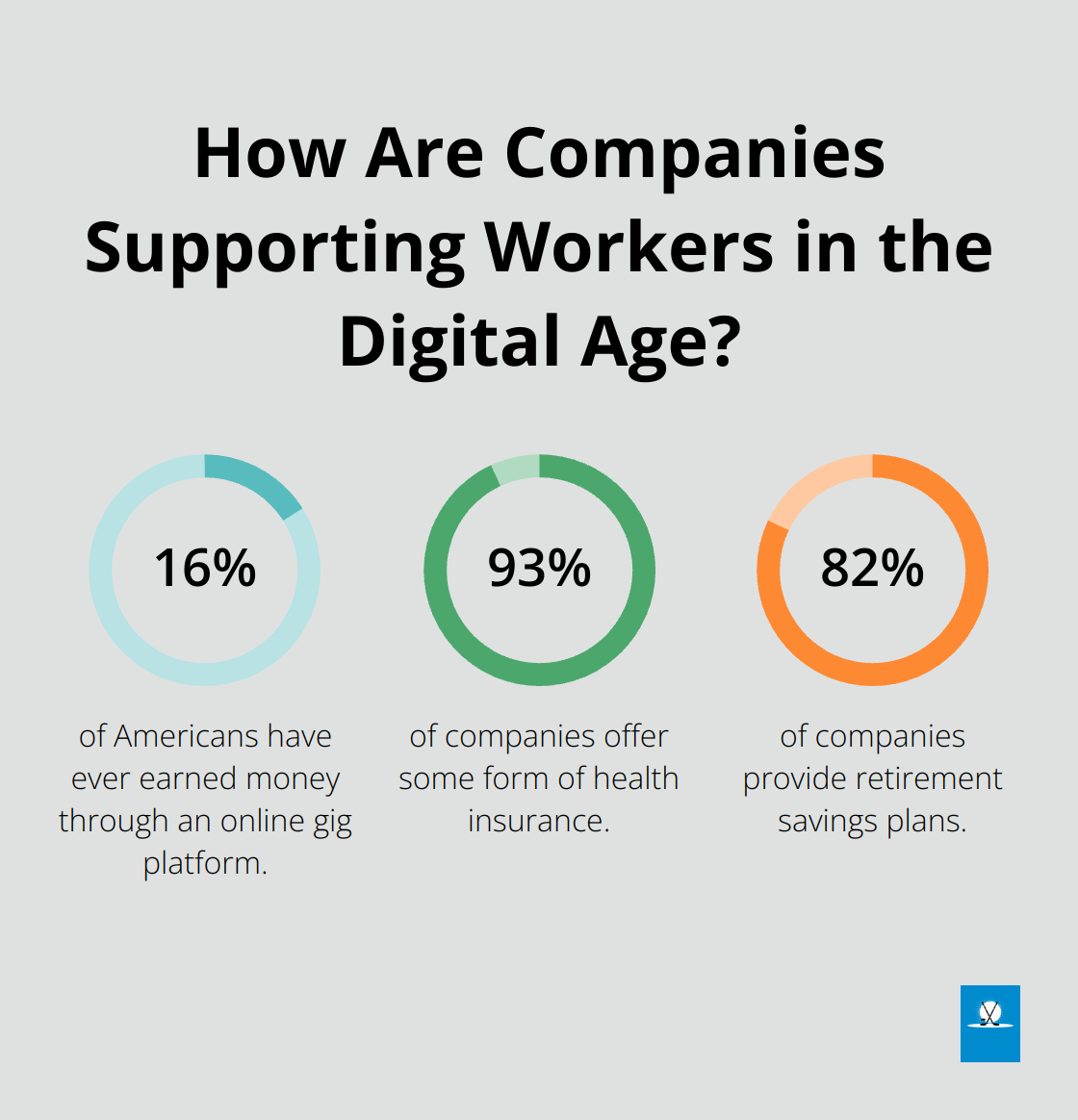

The gig economy provides flexible opportunities to earn extra cash. A 2021 Pew Research Center study found that 16% of Americans have ever earned money through an online gig platform. Popular options include:

- Ride-sharing services (Uber, Lyft)

- Food delivery (DoorDash, Grubhub)

- Task-based work (TaskRabbit, Fiverr)

Select gigs that fit your schedule and skills. If you own a car, ride-sharing could work well. If you excel at home repairs, offer services on TaskRabbit.

Upskill for Better Pay

Investing in your skills can lead to higher-paying job opportunities. The U.S. Bureau of Labor Statistics reports that workers age 25 and over who have less education than a high school diploma had the highest unemployment rate (5.6 percent) and lowest median weekly earnings. Consider:

- Free online courses (Coursera, edX)

- Vocational training programs

- Industry certifications

Focus on skills in high-demand fields like technology, healthcare, or skilled trades. These sectors often offer better pay and more job security.

Maximize Workplace Benefits

Many employers offer benefits that can indirectly boost your income. A 2024 Society for Human Resource Management survey found that 93% of companies offer some form of health insurance, while 82% provide retirement savings plans. Take full advantage of:

- 401(k) matching programs

- Health Savings Accounts (HSAs)

- Employee stock purchase plans

- Professional development allowances

These benefits can significantly increase your overall compensation package and provide long-term financial advantages.

Explore Government Assistance

Government programs can provide important support for low-income individuals. The Supplemental Nutrition Assistance Program (SNAP) helped about 41 million Americans in 2024, according to the USDA. Look into:

- SNAP (food assistance)

- Medicaid (healthcare)

- Housing Choice Voucher Program (rent assistance)

- Low Income Home Energy Assistance Program (LIHEAP)

These programs can free up more of your income for savings and debt repayment. Eligibility criteria vary, so research thoroughly or consult with a social services professional.

Seek Professional Advice

For personalized strategies to boost your income, consider consulting with financial experts. Pro Hockey Advisors offers expert consulting services that include financial planning tailored to your specific situation. Their industry expertise can help you identify unique opportunities to increase your earnings and secure your financial future.

Final Thoughts

Financial planning for low income earners requires dedication and smart strategies. You can build a secure financial future regardless of your starting point through consistent actions and informed decisions. Small, regular steps compound over time, leading to significant results in your financial stability.

Expert advice provides personalized strategies for complex financial decisions. Pro Hockey Advisors offers specialized financial planning services to help optimize your financial future. Our guidance can support you in navigating challenging financial landscapes and creating opportunities you might have thought were out of reach.

Financial success depends on how well you manage your resources, not just your income level. With the right mindset, tools, and support, you can construct a strong financial foundation to serve you for years. Start your journey towards financial stability today-your future self will appreciate the effort.